Voluntary Carbon Market 2026: Key Trends Shaping the Future of Climate Finance

The Voluntary Carbon Market (VCM) is undergoing a major transformation in 2026. Once driven by volume and low-cost offsets, the market is now defined by quality, transparency, and measurable climate impact. As corporate climate commitments mature and scrutiny around greenwashing intensifies, the VCM is evolving into a more credible and structured climate-finance mechanism.

This article explores the most important voluntary carbon market trends in 2026 and what they mean for businesses, investors, and project developers.

One of the most defining changes in the voluntary carbon market is the move away from low-integrity credits toward high-quality, verifiable carbon credits.

In 2026, buyers are prioritizing:

Carbon removal credits over avoidance credits

Nature-based solutions with strong additionality

Credits aligned with Core Carbon Principles (CCP)

Projects with transparent monitoring and long-term impact

This shift reflects a growing understanding that not all carbon credits deliver the same climate benefit. High-integrity credits are increasingly treated as premium climate assets, not interchangeable commodities.

Corporations remain the primary demand drivers in the voluntary carbon market. However, their approach has changed significantly.

Key corporate trends in 2026 include:

Using carbon credits only for hard-to-abate residual emissions

Entering long-term offtake agreements instead of one-off purchases

Integrating credits into broader ESG and sustainability-linked finance frameworks

Improving transparency in climate claims and disclosures

Companies that clearly distinguish between emissions reductions and carbon offsetting are building greater trust with investors, regulators, and consumers.

Carbon credit prices in 2026 vary widely depending on quality and project type. High-integrity credits—especially removals—command significantly higher prices than legacy credits.

Price differentiation is influenced by:

Project type (removal vs. avoidance)

Verification and methodology rigor

Geographic location

Environmental and social co-benefits

This pricing maturity signals a healthier market where credibility and impact are properly valued.

Technology is playing a critical role in strengthening trust in the voluntary carbon market. In 2026, digital Monitoring, Reporting, and Verification (MRV) systems are becoming standard practice.

Key technological advancements include:

Satellite monitoring and remote sensing

AI-based emissions modeling

Blockchain-enabled registries for traceability

These innovations reduce the risk of double counting, improve audit efficiency, and increase confidence for buyers and regulators alike.

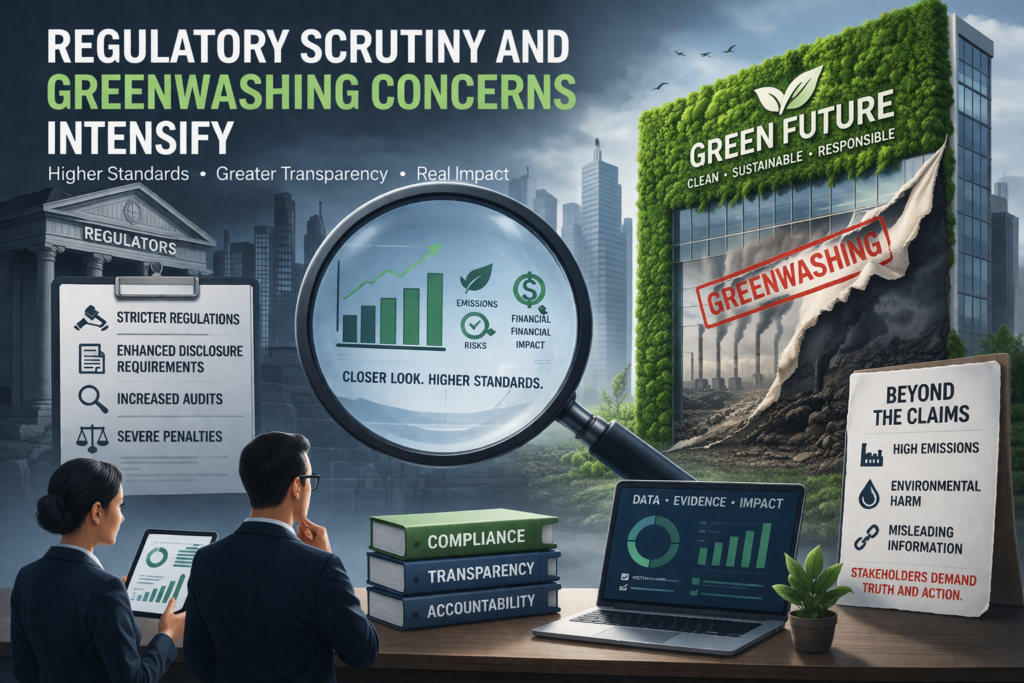

Although the voluntary carbon market operates outside formal compliance systems, regulatory oversight is increasing—particularly around misleading climate and ESG claims.

In 2026:

Regulators are closely examining “carbon neutral” and “net-zero” claims

Disclosure standards are becoming stricter

Companies must clearly justify how carbon credits are used

This environment rewards transparency and penalizes vague or unsubstantiated claims, reinforcing the importance of high-integrity credits.

Nature-based solutions (NbS) are regaining prominence in the voluntary market due to their multiple co-benefits.

High-quality NbS projects deliver:

Long-term carbon sequestration

Biodiversity conservation

Climate resilience

Socio-economic benefits for local communities

In 2026, buyers increasingly favor projects that demonstrate measurable environmental and social outcomes, particularly in emerging markets.

After a period of uncertainty, investor confidence in the voluntary carbon market is gradually returning. Capital is increasingly directed toward:

High-quality project developers

Digital MRV and verification platforms

Carbon market infrastructure and analytics providers

Investors recognize that achieving global climate targets requires scalable, credible carbon-finance mechanisms.

Focus on transparency, long-term partnerships, and high-quality credits aligned with science-based targets.

Robust data, credible methodologies, and strong verification processes are essential for market access.

The strongest opportunities lie in quality-driven projects, technology, and market infrastructure, not volume trading.

The voluntary carbon market in 2026 stands at a critical crossroads. As integrity standards rise and technology improves transparency, the market is evolving into a more mature and trusted climate-finance system.

Organizations that prioritize quality, accountability, and real climate impact will be best positioned to succeed as the voluntary carbon market continues to evolve.

If your organization is exploring carbon credits, sustainability strategy, or climate finance solutions, now is the time to engage with high-integrity markets and credible partners.

Contact us to learn how we can support your voluntary carbon market strategy in 2026 and beyond.

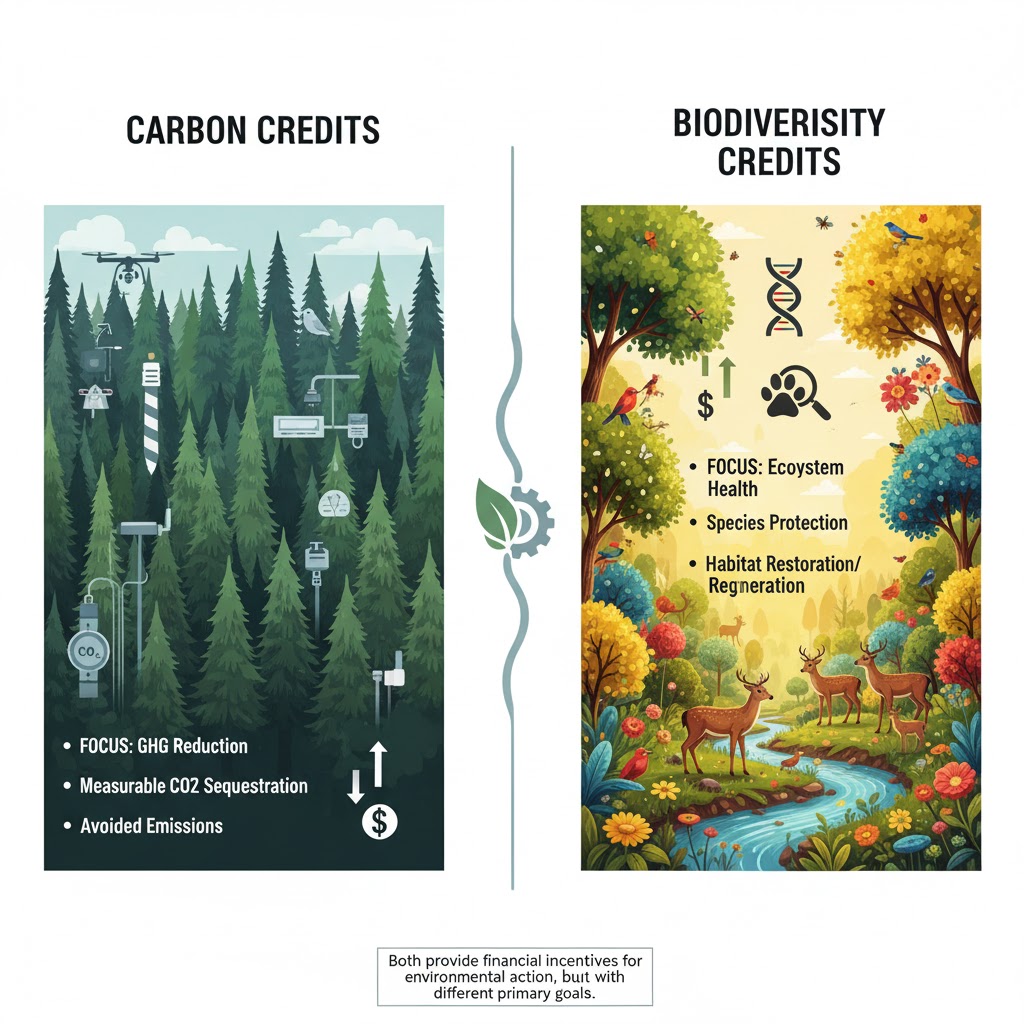

The voluntary carbon market (VCM) is evolving quickly. While carbon credits remain the backbone, a new and exciting trend is gaining momentum in 2025: biodiversity credits. These credits go beyond carbon reduction to protect and restore ecosystems—linking climate action with nature conservation.

Biodiversity credits are units that represent measurable conservation outcomes such as:

* Protection of endangered species.

* Restoration of forests, wetlands, and mangroves.

* Preservation of habitats that safeguard ecosystem services.

Unlike carbon credits, which are measured in tons of CO₂ reduced or removed, biodiversity credits focus on the health and resilience of ecosystems.

According to Ecosystem Marketplace, biodiversity-linked credits could represent a multi-billion-dollar opportunity by 2030.

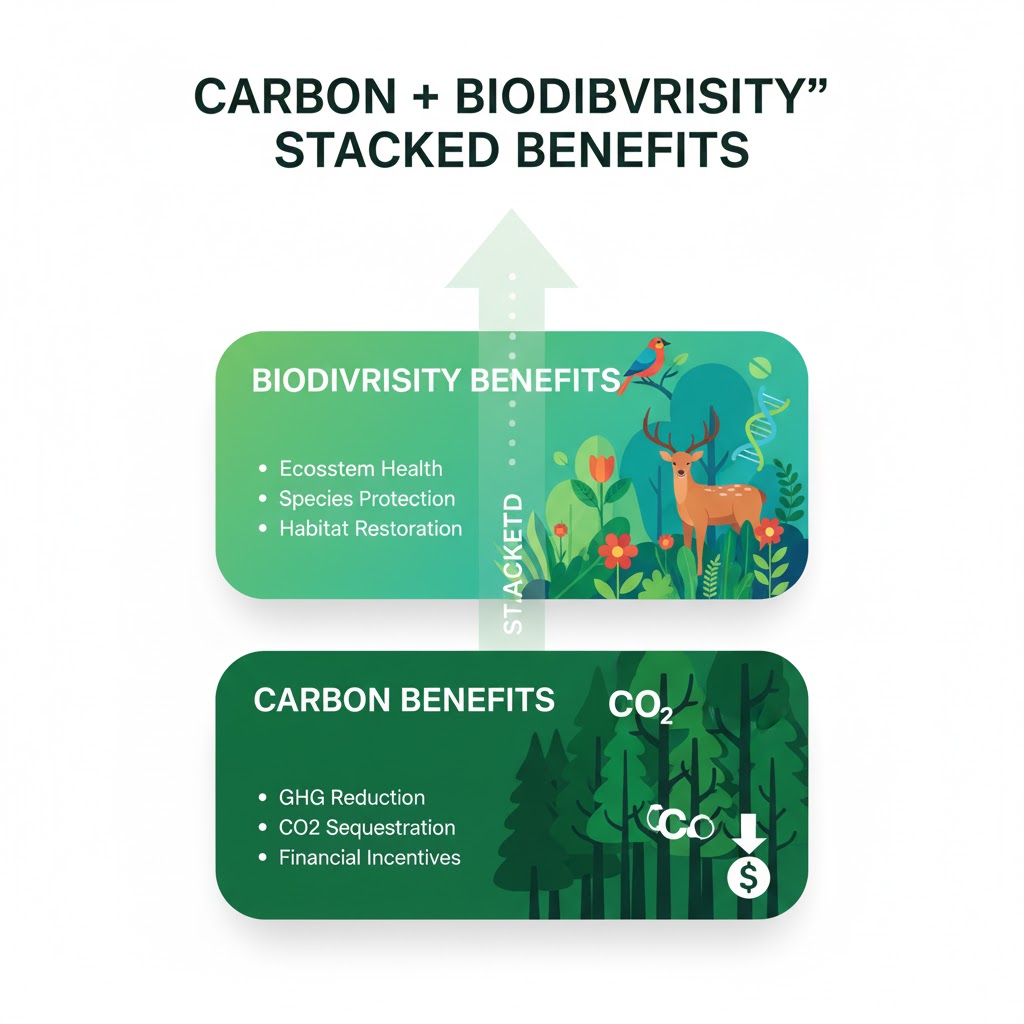

Instead of replacing carbon credits, biodiversity credits are designed to work alongside them.

A forest conservation project can issue both:

– Carbon credits for avoided deforestation.

– Biodiversity credits for protecting species habitat.

This creates a stacked benefits model, rewarding projects for the full scope of environmental value they deliver.

For companies, biodiversity credits offer:

Stronger ESG storytelling – linking climate goals with nature protection.

Brand differentiation – consumers increasingly value biodiversity-positive actions.

Risk mitigation – resilient ecosystems reduce climate and supply chain risks.

Some multinational brands have already begun co-investing in biodiversity alongside carbon projects, positioning themselves as leaders in nature-positive transitions.

The next 2–3 years will determine whether biodiversity credits move from niche to mainstream. Key challenges include:

* Developing robust standards for measurement and verification.

* Avoiding double-counting with carbon credits.

* Ensuring credits deliver real, additional, and lasting benefits.

Still, the momentum is undeniable. As the climate crisis and biodiversity crisis are deeply interconnected, biodiversity credits could become the next big wave in voluntary markets.

Carbon credits may have started the movement, but biodiversity credits are expanding the horizon. For businesses, investing in nature-positive projects isn’t just good for the planet—it’s becoming a strategic advantage.

The voluntary carbon market is no longer just about carbon. It’s about carbon + nature + communities—and biodiversity credits are leading that transformation.

https://www.naturefinance.net/biodiversity-credits/

https://www.weforum.org/agenda/2023/01/biodiversity-credits-nature-carbon/

https://www.naturefinance.net/biodiversity-credits/

https://www.weforum.org/agenda/2023/01/biodiversity-credits-nature-carbon/

https://www.ecosystemmarketplace.com/

As the world shifts towards net-zero planning, carbon removals (CDR) have become a crucial component of corporate climate strategies. However, companies are adopting different approaches to tackle this challenge. In this blog, we’ll explore the various strategies being employed and the implications for businesses.

Science-aligned pathways require deep value-chain cuts and durable removals to neutralize residual emissions. The Oxford Offsetting Principles (2024) recommend a staged transition from avoidance/reduction credits to 100% removals by 2050, emphasizing durable storage solutions like mineralization, DACCS, and BECCS.

Advancements in technologies like Direct Air Capture (DAC) and Bioenergy with Carbon Capture and Storage (BECCS) are critical for scaling up carbon removals. Companies like Climeworks and Carbon Engineering are already leveraging DAC to capture CO2 from the atmosphere, while others are exploring BECCS as a viable solution for negative emissions. As these technologies mature, costs are expected to decrease, making carbon removals more accessible to businesses.

Companies are pursuing different playbooks:

Cautious followers: Limiting action to “beyond-value-chain mitigation” (BVCM) while prioritizing internal abatement.Integrity Frameworks

Recent updates to integrity frameworks provide guidance:

As companies navigate the complex landscape of carbon removals, strategic divergence is expected. However, with integrity frameworks maturing, businesses must prioritize durable removals and credible communication to achieve net-zero goals.

Zipporah is a strategic leader in nature‑based solutions with over ten years of experience driving ecological restoration and climate projects. She joined ClimeTrek in 2022, where she oversees strategic planning, team leadership, compliance, and cross‑departmental coordination. With a first degree in Forestry and specialized training in carbon forestry, climate solutions, and landscape restoration, her career highlights include designing innovative project models and leading carbon project development.

Vinod has been an integral part of ClimeTrek since its inception, initially serving as a Marine Advisor before assuming the role of Head of Operations. With a strong background in conducting environmental compliance & safety audits and managing large-scale projects for ships and shore-based organizations, he brings a wealth of experience to the field of environmental management. His dedication to sustainability, environmental stewardship, and the pursuit of innovative solutions makes him a valuable asset in navigating the complexities of the voluntary carbon market, compliance markets like the EU ETS, and the requirements of organizations in three critical areas: environmental impact, social responsibility, and governance practices (ESG).

Academically I have a masters degree in Environmental Engineering from the University of Algarve in Portugal, and a further masters degree in Climate Change from King’s College London. I have joined ClimeTrek in 2021, working in business development, mainly in project sourcing.

I’ve always been very enthusiastic about Environmental issues, specially climate change, and have experienced first hand its impacts in my hometown in the Algarve, where years of severe draught it’s seriously impacting the life in the region. So for me its very motivating to be involved in the projects that ClimeTrek is developing.

Leena has been a member of ClimeTrek Ltd since its inception. She has over 12 years of experience in office management, accounting, and trading. She oversees company policies and procedures, managing financial and accounting processes, analysing market trends, and facilitating carbon trading transactions that drive positive environmental impact. Leena holds a Bachelor’s degree in Finance and Business studies and a Master’s degree in English Literature. In her free time, she enjoys watching Netflix and reading novels.

DK Balian is the Founder and CEO of ClimeTrek Ltd, a leading climate change and sustainability consultancy and carbon project developer. He has over 27 years of experience in the energy sector and is a sought-after speaker on sustainability and maritime issues. With his Master’s in Maritime Law and practical experience, he is uniquely positioned to advise on climate change impacts from both regulatory and practical perspectives. Through his work, DK Balian is committed to creating a sustainable future for generations to come.

George has spent most of his career in and around oil and gas trading. He feels that his work with Climetrek is some attempt to make amends for his earlier career by undertaking projects to protect the environment rather than continue to destroy it. As a committed family man George enjoys spending time at home but is always curious to travel and experience the lives of others. He has a first degree in Accounting and an MBA.

In his role at ClimeTrek, he manages the Business Development team around project origination with key focus in Asia and Africa around technical and commercial feasibility, as well as devising the business strategies of ClimeTrek. In his spare time, he avidly watches football, and dons on a chef’s hat.

Yucel Kirtman is a qualified engineer with several years of diverse experience working on different projects for energy efficiency, biomass power plants, ORC turbines (Turboden). He worked as an engineer for the last field tests before production of all the tires which are either modified or newly designed in Turkey as well as the approval authority of the reclaimed defected tires. He later moved on to work for Borusan Makine which is the exclusive distributor of Caterpillar and Michelin off road tires in Turkey wherein his responsibilities included managing a team of sales people in different regions, setting the sales target, giving technical support to the team, prepare technical material in Drive train spare parts and Michelin off road tires. In 1998, he started to work for Kordsa which was a JV between DuPont and Sabanci Holding. He was responsible for Nylon 6.6 production, maintenance and utilities

He also started his own company, Kırtman Enerji, which is sales agent of Thermal Energy Inc, Ca.

He was also the director of Hayat Inovasyon which was a startup company established by Hayat Holding managing a marketing team performing service of CNG conversions of diesel truck and buses for big fleets.

Jayshri is passionate climate change and sustainability professional with 15+ years of experience in successfully delivering a wide range of climate change, sustainability, and green energy consulting services. She is experienced in developing leads and complex technical projects with multinational companies and organizations such as the World Bank, UNFCCC and UNIDO.

Banu Sinmaz is Environmental Engineer (MSc) with extensive experience in project management, design of water and waste water treatment plants and solutions, feasibility studies for environmental projects.In her previous roles, she was engaged as an Environmental Engineer, in World Bank Project, Sustainable Cities Project Component – A Consultancy Services for Preparation of Integrated Urban Water Management Plan for Selected Cities for Group 2 (Antalya). She was taking care of comprehensive data collection activities, preparation of IUWM plans and strategies within scope of this project.

Banu’s expertise include sustainable water, wastewater, storm water and solid waste management; water treatment, wastewater treatment, solid waste management solutions, sludge drying, energy from sludge and biomass, pure water demand for tribune line of the power plant, project management, procurement of environmental factories, field jobs of environmental facilities, permission of Environmental Ministry, preparation of feasibility of environmental plants, management of budget, import/export of treatment plant, second hand machinery export.

In addition, she is Occupational Safety Specialist, A-Class (2014).She enjoys travelling, sailing and scuba diving.

Veethika is a climate policy specialist managing ClimeTrek’s carbon offset trading desk in London. She has experience in community development implementation and systematic research on environmental certification and climate finance. She is passionate about market-based mechanisms and synergistic systems addressing environmental externalities. In her free time, she enjoys reading and traveling.

Sachin holds a decade of progressive experience working in the HR domain with Industries like Business Process Outsourcing, Insurance, and Think tanks. His areas of expertise include recruitment, induction and orientation, attendance management, performance management, policy designing, employee benefits, and statutory compliances. He is compassionate, energetic, result-driven, and a creative thinker.

He did his master’s in Human Resource Management and Bachelor’s in commerce.

Jing is a part-time Carbon Market Intern at ClimeTrek’s London office. She is currently pursuing her MSc in International Social and Public Policy at LSE. Her dissertation focusses on the development of grassroots social businesses in China, with a particular emphasis on local public policies. Prior to this she studied Social Sciences at Waseda University, Japan.

She has experience with impact analysis of ESG and CSR projects from her past internships in China. Jing is interested in carbon offsetting markets and projects related to sustainable development and community benefits, especially in East Asia.

Her hobbies include learning new languages, baking and travelling..

Holding a BSc in Biological Sciences from the University of Exeter and an MSc in Climate, Change, Development and Policy from the University of Sussex, Inigo’s academic choices were inspired by his commitment to protecting the natural world and an awareness of the challenges it faces.

On the professional front, he has the experience of working as a Research Assistant focused on conservation, research, and environmental education of endangered species for Ecology Project International (EPI) at the Pacuare Reserve in Costa Rica.

Joel is a Nigerian Qualified Lawyer, and an applicant to the Roll of Solicitors of England and Wales. He holds a post graduate specialist degree in International Commercial and Maritime law from Swansea University, Wales, UK. He has strong interests in, and over 18 years cumulative cognate experiences as a legal service provider in the areas of Contracts Management, Commercial Legal Advisory, Regulatory and Corporate Compliance and Litigation.

Joel is an avid reader, he also loves to watch and play football.